![]()

What could have been on his mind? 41 year old, David Kellerman, was found hanging in the basement of his Vienna, VA home early this AM. Police responded to a 4:45AM 911 phone call, but declined to say who had placed that call.

Kellermann, 41, and a 16-year veteran of Freddie Mac, had been the company’s CFO since September, after a government takeover of the company following the housing crisis. County records show the large home in Hunter Mill Estates was worth about $900,000.

~~~Kellermann was named acting chief financial officer in September 2008, after the resignation of Anthony “Buddy” Piszel, who stepped down when the government took over.

According to securities reports filed in March, Kellermman was to receive an $850,000 bonus.

Kellermann owned 43,000 shares of Freddie Mac stock last summer, worth about $395,000. As the company’s stock plummeted from $9 a share in July to 80 cents or so this morning, he had slowly sold off some shares, for pennies on the dollar. His holdings of 38,861 shares, as of April 11, were worth $30,000, according to ABC News’ calculations of Security and Exchange Commission filings.In filings with the SEC in March, Freddie Mac said it had entered into a pact with Kellermann and two other company executives to protect them from liabilities and expenses in connection to any threatened or pending lawsuits. The agreement, which kicked in retroactively from the time of the government takeover, would not protect the officials from willful criminal misconduct.

In an SEC filing from September, Freddie Mac disclosed that it received a federal grand jury subpoena from the U.S. Attorney’s Office for the Southern District of New York seeking information about the company’s accounting, disclosure and corporate-governance procedures. The subpoena was withdrawn, and the investigation was taken over by the U.S. Attorney’s Office for the Eastern District of Virginia.

Before he was named acting CFO, Kellermann served as senior vice president, corporate comptroller and principal accounting officer.

What can we take away from this INRE motives? Was Kellermann… father of a young five year old daughter… panicking about possible criminal charges?

Or was he worried about publicity leading to ACORN style public harrassment? According to the New York Times version of the story, Kellerman had to hire a security firm after reporters started showing up to question his $800K bonus.

Mr. Kellermann, 41, had been Freddie Mac’s chief financial officer since September. He was named to the position when the federal government seized the company and ousted its top executives last fall. In recent weeks, according to neighbors and company officials, Mr. Kellermann had received a bonus of about $800,000. Such bonuses — which totaled $210 million for executives at Freddie Mac and its sibling company Fannie Mae — caused some controversy earlier this month, and some lawmakers called for them to be rescinded.

According to neighbors, Mr. Kellermann hired a private security firm after reporters came to his house to ask about his bonus.

Some neighbors told The A.P. that Mr. Kellermann had lost a noticeable amount of weight under the strain of the job, and some said they suggested to him he should quit to avoid the stress.

Also on Kellermann’s plate was “tense” negotiations with federal regulators over public disclosures. The Freddy execs wanted to emphasize to investors that the company was being run for the benefit of the government, rather than shareholders.

In contrast, the regulator – Federal Housing Finance Authority – wanted to play that notion down.

Freddie Mac ultimately reported that it made changes to business practices to help the government that “have increased our expenses or caused us to forgo revenue opportunities.”

OpenMarket.org has more on this disguised “disclosure”, and in fact has some serious criticism of the government’s handling (yes, including this administration) of the financial crisis.

Since the government takeover, the GSEs have been in an ambiguous balancing act of private/public status. The FHFA has full authority to direct the company’s affairs after the take over, but the Obama administration is reluctant for a full government nationalization, as this would end their pursuit of profits and the requirement that they make regulatory disclosures for the benefit of private investors.

From a linked WaPo article March 27th, the dual between the Freddie execs involved in the negotiations about the public disclosure reporting centered around how much should be disclosed about the government’s role in Freddie’s losses.

Federal officials who took over Freddie Mac stopped short of nationalizing the company, leaving it partly in private hands. This means Freddie still has to answer to investors and file financial disclosures.

But when Freddie Mac’s executives concluded a few weeks ago that they had to disclose that the government’s management of the McLean company was undermining its profitability and would cost it tens of billions of dollars, the firm’s regulator urged it not to do so, according to several sources familiar with the matter.

Freddie Mac executives refused to bend. The clash grew so severe that they threatened to go to the Securities and Exchange Commission, which oversees corporate disclosures, to secure a ruling that the regulator’s request was out of line. The company’s regulator backed down, the sources said.

~~~Now these unresolved questions about Freddie Mac’s status are driving the dispute about what it should disclose as a publicly traded company listed on the New York Stock Exchange.

As Freddie Mac executives were preparing their annual 10-K financial disclosure this month, they reported that carrying out the Obama administration’s housing plan would cost $30 billion this year. That sum would have to be covered by the Treasury Department. The federal government has pledged to cover $200 billion each in losses for Freddie Mac and Fannie Mae, of which the pair have asked for about $60 billion.

The housing agency asked that the cost of the program be withheld and that the firm soften language describing how government management was undercutting profitability, according to sources.

The Freddie execs… presumably including now deceased Kellermann. were ready to take the regulator to tasks on what what was their requirement to disclose what the government regulator wanted them to withhold…. that the new O’admin plan was about to plunge them into further jeopardy. What the execs ultimately did agree to do was work with the regulator on the “language” that softened the truth.

What Freddie was warning was that it’s mandated participation in Obama’s HASP debacle for “saving homes”… which as I dissected in my February 19th post as tandamount to taxpayer financed buyouts of mortgage points for some, and refinancing into a five year government sponsored ARM loan … would incur a $30 bil initial pre-tax charge that would grow exponentially with the economic decline, and lead to the need for future taxpayer cash infusions.

The main way that the government is c ausing Freddie to incur losses is by requiring it to play a central role in the Obama administration’s Homeowner Affordable and Stability Plan, a $75 billion effort launched this month. The program aims to restructure mortgages that struggling borrowers cannot afford, bolster the sagging housing market and bring down interest rates on home loans.

The Obama plan will require Freddie Mac to modify mortgages, which entails reassessing the value of loans and marking them down to current market price. The company must then record a charge to reflect these decreased values. Based on Dec. 31 figures, Freddie Mac said it would incur “an initial pre-tax charge” of $30 billion. That number could grow as the economy declines and would have to be offset by infusions of government capital.

“These initiatives are likely to have a significant adverse effect on our financial results or condition,” Freddie Mac warned in its regulatory disclosure.

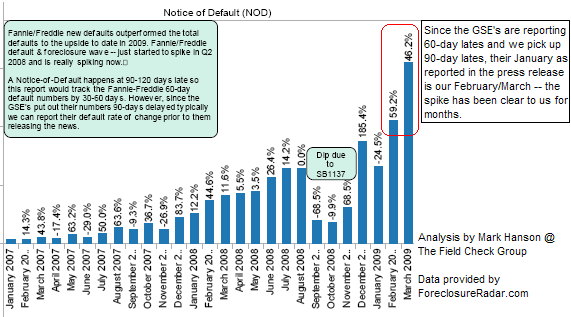

Lending creditability to the GSE’s financial state in the wake of the government/exec disclosure battles, Bloomberg reports today of the rising mortgage defaults occuring at Fannie and Freddie.

Fannie Mae and Freddie Mac mortgage delinquencies among the most creditworthy homeowners rose 50 percent in a month as borrowers said drops in income or too much debt caused them to fall behind, according to data from federal regulators.

The number of so-called prime borrowers at least 60 days behind on mortgages owned or guaranteed by the companies rose to 743,686 in January, from 497,131 in December, and is almost double the total for October, the Federal Housing Finance Agency said in a report to Congress today.

Of all borrowers who ended up in default, 34 percent told Fannie and Freddie they were earning less money, about 20 percent cited excessive debt as a reason for missing mortgage payments, and 8.1 percent blamed unemployment, FHFA said.

Keep in mind, that “FHFA said” is the same FHFA that was fighting with Kellermann and other execs to mask the government’s role in Freddie’s profitability…

So where does this leave us with Kellermann’s death? Was he in fear of criminal prosecution? He certainly didn’t appear to be financially destitute.

There’s the darker, conspiracist side of things. Self-admitted white supremecist, Hal Turner of the Turner Radio Network blog, is proudly taking twisted credit for inciting followers to violence… “lynching” Kellermann in retaliation for for the financial crisis. I absolutely refuse to link his site here… not a nanobyte of hotlinks from me. In fact, just typing his name, and I feel the need for a bath.

I do believe this man is equally despised by conservatives and liberals. But it’s more than ironic to see a neo-nazi siding with the deeds and actions of ACORN, and their assault upon CEOs.

I’m not sure what the story is behind Kellermann’s death… suicide from pressure or fear of exposure? Or could it possibly be murder? But it is a scenario fraught with intrigue, money, power and corruption already.

Vietnam era Navy wife, indy/conservative, and an official California escapee now residing as a red speck in the sea of Oregon blue.

This is so sad! No one should ever be driven to this! IMHO the really guilty parties are in CONgress – taking all their raises, perks and whatever. This really tees me OFF!!!

yes, it is sad that he took his life having a family. But I’d resist blaming anyone or circumstances for his suicide. Suicide is an inside job. Its easy for those outside of him to lay blame to external circumstance. Family members do that a lot because they cannot accept that something was wrong with him. Of course there are “justifiable” reasons to commit suicide (9/11 and the Twin Towers comes to my mind). But in the long run this man made a choice and I feel for his family, regardless of the surrounding circumstances.

Sorry, but this does not pass the smell test. No evident financial problems, young, young family, why would he off himself?

I agree with Mike. Something fishy here and I guess we will have to wait and see what the investigation uncovers.

If he hired a security firm there may have been threats against him but I doubt they came from ACORN which has been milking both Fannie and Freddie thanks to the Dems that have turned both mortgage giants into piggy banks for left wing causes.

Did the guy leave a suicide note?

Just like the person who was murdered that had knowledge of the passport “breeches” of Obama during the campaign.

I feel empathy for the family, for sure.

I also think it smells fishy as he certainly had a lot of people angry at him. I also can see that suicide is not implausible either. But, I’m sure they will investigate this and NOT brush this under the rug (I say with uncertain faith!)

Why do these things (possible murders and suicides) seem to happen mostly when a Democrat is in The White House?! Sorry, not feeling too non-partisan right now. If I’m wrong, then I’ll sit corrected.

Thanks for pointing that out Karma. Little has been said or reported on Lt. Quarles Harris Jr. I pointed out on another blog that had this “suicide” posted that I thought perhaps conclusions were being jumped to a bit too quickly.

I wonder if Hillary Clinton was anywhere near him? It seems that people are mysteriously dying like in the Clinton Administration when scandels popped up.

i sent a comment earlier… think it got caught in spam filter. anywhooo…

does anybody know if Kellermann was trying to quit smoking?

My fault Reeko, saw it in spam and the smoking stuff made me think it was indeed spam…..if you want to repost it I’ll put it up.

Don’t find it, reeko. What’s your point? That he was nicotine challenged and that lead to suicide?? Can’t go there myself. Sorry. Grumpy and eating everything that is digestable and not nailed down, yes. Suicide? nope

i was trying to point out some salient facts about suicide in and of itself, and the MSM dire need for “reasons” which, for those who’ve had to deal with it, sometimes there just ain’t…

now back to the media…

(factoid 1) Chantix and Zyban are known to cause a spike in suicidal behaviors, and millions of dollars have been already awarded to plaintiffs over that KNOWN fact.

(factoid 2) the Pentagon had a max-effort stop smoking campaign last year, culminating in the 20 Nov 2008 Smoke Out day. DoD pharamacies already banned both Chantix and Zyban early last year from any “aircrew or missile crews” for the specific reasons of erratic behavior, yet in last year’s anti-smoking campaign, according to one source, these very same drugs were dispensed “like candy” to anybody else. their rationale (can’t seem to google it right now) was that the “results outweighed the risks” of SUICIDE! in other words, dead bodies are OK to the anti-smoking Nazis. (full disclosure: i quit a 30 yr pack-a-day habit a couple years ago. cold turkey. but i still feel solidarity with my smoking friends.)

(factoid 3) Law Enforcement Officers do not pronounce why they think somebody committed suicide. they are only liable to look at apparent suicides for signs of foul play, in order to rule out any homicide or “assisted” suicide. although hangings appear to be self-inflicted, LEO are duly bound to rule anything else out. however, once it becomes clear there was no suspected foul play they try NOT to attempt any other explanation for a suicide. even if the LEO are bonified head-shrinks, any professional who has worked with these types of cases will tell you, delving into the psyche of a suicide victim (and i disagree with the term “victim” – only using it here for clarity) is more often than not an excercise in best-guessing.

(factoid 4) media apparatchiks have recently spent volumes of ink and wavelength trying their best to disregard any obvious links between the spike in military suicides to the spike in the use of smoking cessation drugs – pushed BY the military. instead, they’ve loudly proclaimed that it MUST be cause only from PTSD brought on by Bush’s War/GWOT and they’ve stated their flimsy case so vociferously that the ersatz connection has now passed on into the public realm of reality (ie: repeat the lie often enough… etc.) much like the drug-addicted suicidal Vietnam vet icon – which was also proven to be a complete fictional stereotype – but is now accepted as fact.

so what does the above have to do with Kellermann? reflect on this ABC News headline in January:

Econo-cide: Financial Woes Turn Deadly

http://abcnews.go.com/Business/Economy/story?id=6765383&page=1

and yesterday:

Freddie Mac CFO’s Death: Was it Econocide?

http://www.gawkk.com/freddie-mac-cfo-s-death-was-it-econocide/discuss

ad nauseum…

the very fact that ABC would use the term “econo-cide” with Kellermann leads me to believe it was something else. my question is therefore valid:

was he a smoker? and was he trying to quit? if not, then plz disregard my ranting. LOL 😉