![]()

by Don Surber

As I watched the sudden collapse of the Silicon Valley Bank, I marveled once again at how a geezer’s administration run by tokens of diversity can wreck the economy by turning mundane functions — say, unloading transport ships — into extraordinary catastrophes, such as a supply chain backlog.

Train wrecks happen, sure, but it takes a special innate incompetence to have the EPA set fire to the toxic contents spilled over the tracks in East Palestine, Ohio, sending a black cloud into the air that was seen for miles around as it spread the danger over hundreds of square miles.

I am awestruck by the ineptitude of a Department of Transportation that spends billions of dollars not to build roads but to destroy them in the name of fighting racism.

The return of inflation after a 40-year hiatus tops the list of Biden’s calamities. Thus far the administration’s answer is to keep borrowing and spending as if there is no tomorrow in the fervent and erroneous belief that this will make it go away, when in fact all it does is fuel inflation.

No idea is too kooky for these Ivy League-educated idiots. The Los Angeles Times reported, “How white and affluent drivers are polluting the air breathed by L.A.’s people of color.”

The story said, “Angelenos who drive less tend to be exposed to more pollution.

“It may sound like a paradox, but it’s not. It’s a function of the racism that shaped this city and its suburbs, and continues to influence our daily lives — and a stark reminder of the need for climate solutions that benefit everyone.”

The people who live near freeways are poor and the LA Times presumes they all are people of color. Look for Biden and his Band of Bimbos to destroy freeways in Southern California in his second term and turn them into more camps for the homeless. This will continue until liberals decide that because most homeless people are white that homelessness is white privilege and start destroying the camps.

Behind every disaster, of course, is a token that Biden appointed to be the first fill-in-the-blank.

The smoke-’em-if-you-got-’em EPA is run by its first male black administrator. The first woman Treasury secretary is overseeing the return of inflation. The first Homeland Security secretary born in Cuba gave us the biggest border crisis in American history. The first Latino Health and Human Services secretary gave us a shortage of baby formula.

And of course, the man behind the supply chain problem, the airline crisis, and the destruction of highways is the first homosexual Cabinet member not named Ric Grenell.

The collapse of the Silicon Valley Bank is the shiniest example of failure. For 4 decades, SVB financed the mining of tech-industry gold. Biden demolished it in two years.

Reuters reported, “Based in Santa Clara, the lender was ranked as the 16th biggest in the U.S. at the end of last year, with about $209 billion in assets. Specifics of the tech-focused bank’s abrupt collapse were a jumble, but the Fed’s aggressive interest rate hikes in the last year, which had crimped financial conditions in the startup space in which it was a notable player, seemed front and center.

“As it tried to raise capital to offset fleeing deposits, the bank lost $1.8 billion on Treasury bonds whose values were torpedoed by the Fed rate hikes.”

Those rate hikes were to cure the inflation that the first woman Treasury secretary resurrected from the dead.

Without any sense of irony, White House Council of Economic Advisers chair Cecilia Rouse told Fox, “Our banking system is in a fundamentally different place than it was, you know, a decade ago. The reforms that were put in place back then really provide the kind of resilience that we’d like to see.”

Need I say she is the first black woman to serve in that office? Need I also point out that the collapse actually shows those alleged reforms failed?

California regulators shuttered SVB after they noticed depositors suddenly withdrew $42 billion from the bank on Thursday.

On Sunday, CNBC reported, “U.S. regulators on Sunday shut down New York-based Signature Bank in a bid to prevent the spreading banking crisis.”

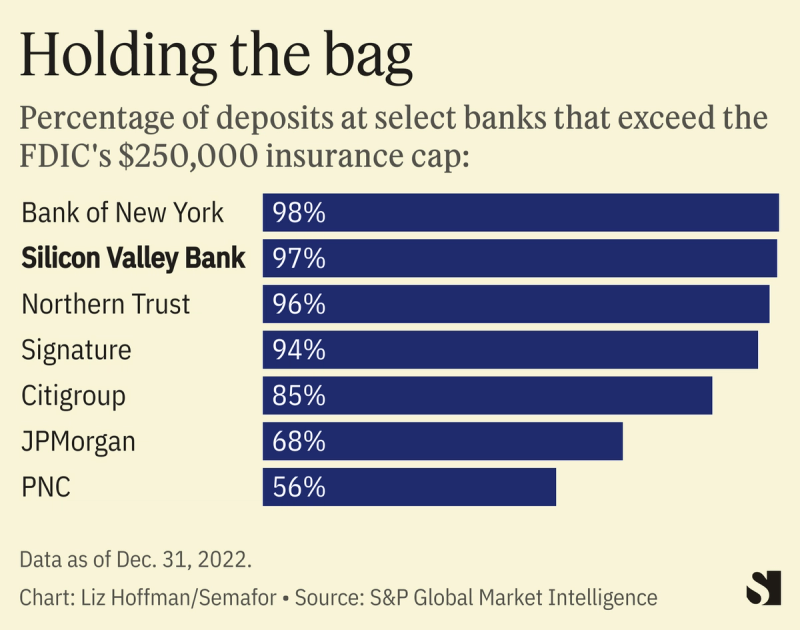

I believe it is too late to prevent the inevitable. Too many banks are holding onto too many deposits that are uninsured. 94% of Signature’s deposits were uninsured. The dirty little secret is FDIC insured deposits are small at big banks.

56% of PNC’s deposits are uninsured. 68% at JPMorgan. 85% at Citigroup. 98% at Bank of New York. Who will cover for them?

Don’t think it can’t happen to them because it will. SVB was a winner until Biden came along.

Bill Biggerstaff and Robert Medearis founded SVB in 1983 as a conduit for venture capitalists to invest in Silicon Valley startups. The bank’s fortunes rose with the rise of companies founded in the Bay Area. Later it expanded into real estate and wineries. In retrospect, it was destined to succeed because the bank helped finance the economic colossus we call Silicon Valley. It is to the 21st century economy what Detroit and Pittsburgh were to the 20th century’s economy.

The money poured into SVB like it did to Studio 54 in the coke-craven 1970s and 1980s. Unlike that New York disco, the money was legal and not kept in garbage bags, but the amounts deposited were outside the FDIC’s coverage.

97% of its deposits were uninsured. As the big banks spin this as the fault of the FDIC, remember they seek insurance coverage of money they did not insure. SVB paid insurance premiums for only 3% of its deposits. That is all the money it is entitled to. These are the rules the banks wanted because if the banks wanted the coverage, they would have gotten Congress to cover them.

If you go uninsured and you wreck your car, you pay to fix it. The same should be true with bank deposits. I get that the feds limit their insurance to the first $250,000 of each depositor’s money. But why isn’t there a secondary insurer? Why don’t the Aflac duck and the Geico gecko get together and provide insurance for deposits above $250,000? They could hire Flo to pitch their insurance.

We know why not. The rich already have insurance on their uninsured balances. It is called Congress. The rich know if they apply enough pressure from a foolish public, the rich always can get another bailout.

However, the word bailout freaks out the public. Enter the Federal Reserve — you know, the people whose rate hikes caused SVB to fold. Taxpayers won’t cover the uninsured deposits. The Federal Reserve will.

The Fed said, “To support American businesses and households, the Federal Reserve Board on Sunday announced it will make available additional funding to eligible depository institutions to help assure banks have the ability to meet the needs of all their depositors. This action will bolster the capacity of the banking system to safeguard deposits and ensure the ongoing provision of money and credit to the economy.

“The Federal Reserve is prepared to address any liquidity pressures that may arise.

“The additional funding will be made available through the creation of a new Bank Term Funding Program, offering loans of up to one year in length to banks, savings associations, credit unions, and other eligible depository institutions pledging U.S. Treasuries, agency debt and mortgage-backed securities, and other qualifying assets as collateral. These assets will be valued at par. The BTFP will be an additional source of liquidity against high-quality securities, eliminating an institution’s need to quickly sell those securities in times of stress.

“With approval of the Treasury Secretary, the Department of the Treasury will make available up to $25 billion from the Exchange Stabilization Fund as a backstop for the BTFP. The Federal Reserve does not anticipate that it will be necessary to draw on these backstop funds.”

So magically — without authorization or funding from Congress — the Fed on a Sunday afternoon created a $25 billion spending program because no one in the press or Congress will protest. It just does what it wants when it wants as it continues to prop up an economy gutted by cheap Chinese imports. That this program will only encourage more folly by bankers goes without saying.

{kind=link}

A top thing that did them in was buying a huge amount of treasuries at low interest rates over the last 2 years. Those bond prices collapsed with the FED rapidly jacking up rates.

But, close on that issue’s heel’s was that they used “woke” instead of real risk assessment to judge who to loan to.

Big mistake.

Lovely that the management could run their woke enterprise into the ground yet still walk with a golden parachute while joe promises to make their customers whole.

Solyndra, anyone?

Self insurance is keeping it in a home safe, there was no bank offering a higher interest rate than inflation, not bonds not CDs. The banks were just a parking place to digitally move your money for bills and purchases.

But with the interest paid on loans they built many branches.

In standard portfolio construction, bonds are generally regarded as the steady but boring components. Within the world of bonds, US Treasuries occupy the highest rung of credit quality and, in normal times, the very definition of staid, “risk-free” holdings, because the US Government pays back its debt.

But, since 2021, with the biggest explosion in inflation in four decades, the near-term volatility of Treasuries rocketed higher. Consider, for example, that a Two-Year Treasury note started the Biden administration with an interest rate near zero. Even though the post-pandemic economy was roaring back to life, during the “Trump Boom 2.0,” inflation was negligible. As Biden took office in January of 2021, Two-Year Treasury Yield stood at 0.13%. But last week…2 Year Yield hit 5.00%, the highest level since 2007. That rapid ascent of short-term rates — almost 40 times higher than just 26 months ago – produced a meltdown in Bond prices throughout 2022.

Bond prices move inversely to yield. So, as interest rate soared, bond prices collapsed. Longer-term Treasuries lost 18% in 2022, the worst year ever — and nearly doubling the losses of the second worst year ever.

How stable are Treasuries normally?

Well, over the last century, T-Bonds only lost 1% or greater in 16 years total out of 100, per data compiled by the NYU Stern School of Business. Even worse, bonds got clobbered in 2022 concurrent with stocks, an incredible rarity in capital markets. In a normal business cycle, when capital markets function properly, a terrible stock year like 2022 compels a “flight to safety” demand for bonds. Consequently, investors expect bonds to act as effectively insurance against more volatile equity holdings.

Biden, Bonds, and Bank Failures

The ravages of Inflation…

STEVE CORTES

MAR 11

∙

SVB collapse: Bank fallout shines spotlight on $620 billion hole in banking sector

Fallout from the Silicon Valley Bank collapse has directed attention to a $620 billion ticking time bomb in the banking system that has the potential to spell doom for the financial system.

SVB’s meltdown was partly caused by a chasm between its assets and what they were worth in the market. Eventually, SVB sold some of those assets, spooking investors and triggering a run on the bank. But SVB isn’t alone, as banks across the United States were sitting on $620 billion in unrealized potential losses at the end of last year, per the Federal Deposit Insurance Corporation.

SILICON VALLEY BANK COLLAPSE: U.S. OFFICIALS REPORTEDLY WEIGH BACKSTOPPING DEPOSITORS

That hole illustrates why authorities at the Federal Reserve, the Treasury Department, and the FDIC were so eager to stave off contagion or panic spread from SVB’s demise across the banking sector.

The reason for this predicament is that banks compiled a plethora of bonds and treasuries during times when interest rates were hovering near zero. But now, the Federal Reserve has begun jacking up rates in an effort to combat inflation, which has caused many of those assets to plunge in value.

This is because higher interest rates mean that new bonds accrue higher rates of returns for investors. As a result, older bonds have comparatively lower rates of return, rendering them less desirable for investors and therefore triggering a plunge in the value of older assets.

$620 billion of unrealized losses, overall equity 2.2 trillion. If a run on the banks would happen it could be fatal even for several large US banks like JP Morgan and Citi. This crisis isn’t over. The US Treasury simply bought some time. pic.twitter.com/2xNvfIrN9b

https://12ft.io/proxy?q=https%3A%2F%2Fwww.washingtonexaminer.com%2Fpolicy%2Feconomy%2Fsilicon-valley-bank-collapse-spotlight-620-billion-hole

Benedict Biden Claims ‘US Banking Is Safe’ as Shares of First Republic Bank Crash 74 Percent

Silicon Valley Bank on Friday Paid Out Annual Bonuses to Eligible U.S. Employees, Before the Bank Collapsed and Was Seized

And now they want the deplorables to bail them out. Uh, no, not interested

The federal government ISN’T bailing out Silicone Valley Bank. The FDIC is backing insured accounts. The corporation and its stockholders are screwed.

Who pays the fees that fund the FDIC?

Taxpayers—the majority of whom don’t want a run on banks that would leave their money worthless and the entire economy in ruins.

The FDIC has about half of the 264 billion deposits at SVB

03/11/23 – Watchdog: Silicon Valley Bank’s Collapse Traced Back to Trump-Republican Roll Back of Dodd-Frank –

Be wary of revisionist history from Republicans in Congress today amid the sudden collapse of Silicon Valley Bank, “the largest U.S. banking failure since the 2008 financial crisis and the second-largest ever.” In fact, conditions for the collapse were made perfect under Republican-sponsored, Wall Street-pushed bill signed into law by President Trump in 2018 that severely watered down risk-assessment rules for two dozen of the largest banks that collectively hold trillions of dollars in assets and received tens of billions of dollars in TARP bailout funds after the 2008 financial crisis. These banks include Silicon Valley, whose CEO lobbied hard for the Dodd-Frank roll back – which ironically led to his own bank’s demise and a questionable decision to dump millions of dollars in stock in the company just two weeks ago.

–

Despite warnings at the time from consumer advocates including Accountable.US that removing Dodd-Frank safeguards invited the same kind of risky behavior that led to the financial crisis, the so-called ‘Economic Growth, Regulatory Relief, and Consumer Protection Act’ passed with unanimous Republican support after taking millions of dollars from the financial industry.

–

This mess was left behind by Congressional Republicans and the Trump administration who were too deep in the big banks’ pocket to care about the consequences of gutting financial industry oversight. The chickens came home to roost this week in the Republican war against Wall Street reform and consumer financial protections.

–

Under the Republican roll back of Dodd-Frank, major institutions like Silicon Valley that oversee trillions of dollars in assets have far less of a burden to prove they can stay standing in difficult economic times. This predictable disaster should give serious pause to the current MAGA House majority who are pursuing further roll backs of consumer financial protections after taking money hand over fist from Wall Street banks – but don’t count on it.”

Basically, Democrats put up guard rails after the 2007-2008 financial debacle, and the GOP tore them down after Trump took office.

Basically, you’re full of shite.

Out of 37 Democrats, 16 voted FOR S. 2155.

Exactly what regulations that were torn down would have saved them?

Come on Im sure you know

It was the metal guardrails vs wood.

Total bullshit. This is bidens fault

Bromides and platitudes. No facts

Were the guardrails metal or wood?

03/13/23 – Trump’s Rollback of Dodd-Frank Regulations Directly Led to the Silicon Valley Bank Failure –

The new republic, a far left wing rag

03/13/23 – DeSantis and other prominent Republicans blame ‘woke’ politics for Silicon Valley Bank’s collapse instead of bankers miscalibrating risk –

Moronic.

From the same morons who call you a “white supremacist” when you point out their errors.

Dismissed.

So it was Trump running the bank he was making shitty china loans…I see.

He also prevented this bank from hiring a risk assessment officer .

Hey, the right is insisting it’s all Biden’s fault, and making moronic claims that their “woke” boogeyman is somehow responsible.

What we should really be asking is why investment banks even exist. People deposit money in banks for safety—not to be paid paltry interest rates while somebody else puts their money at risk. The repeal of the Glass-Steagall Act set the stage for all of this greed-driven bullshit. People who believe in the conservative values of work and saving for the future are made to feel like idiots by those who borrow and gamble.

Yes, “Biden” is to blame, “Biden” being the name we call the collective federal government now that is too corrupt and too unconstitutional to function properly.

The notion of “blame” is something fed to the Left almost exclusively, as talkshow hosts and talking heads used this to get votes from people who have no reason voting the first place.

The world was at peace during Trump. Real jobs, real unemployment, and real economy.

Now that’s gone.

How long do you think your voters will really buy all your “blame” nonsense?

When they have no money for rent, or to feed their kids?

You should know the dangers of crowds, greg, since that’s what your Party has been using for decades.

Nothing is Bidens fault hell he cant even follow Zelensky around Kiev with out getting his hand held.

Who ever has the hand up the Biden puppet ass is to blame.

Hiring execs that ran the last melt down whos brain fart was that?

“Trump Curse? Signature Bank Fails Two Years After Bank Closed President Trump’s Accounts Over January 6 Riot”

Like how you blamed the 2008 financial disaster on then President G.W. Bush?

More bullshit

For roughly 77 hours, between noon ET on Friday and 6pm on Sunday, a chorus of Silicon Valley bigwigs and elected leaders called vocally for uninsured depositors of Silicon Valley Bank to be made whole — to be bailed out by the federal government. In the end, they got what they wanted.

Why it matters: The Biden administration is pushing back hard on the idea that this was a bailout. “No losses associated with the resolution of Silicon Valley Bank will be borne by the taxpayer,” says the official statement from Treasury, the Fed, and the Federal Deposit Insurance Corporation. Many won’t be convinced.

How it works: When a bank fails, depositors are made whole by the FDIC insurance fund. The insurance only covers deposits up to $250,000, although there are plenty of workarounds that allow depositors to effectively buy much more FDIC insurance than that.

In the cases of SVB and Signature Bank, FDIC insurance will now cover all depositors, regardless of size. The FDIC insurance fund — which is funded by a levy on bank deposits — stands at roughly $125 billion.

It’s worth noting this is nothing radical or new. Uninsured depositors have been paid out in full in every bank failure in living memory, with just one exception — IndyMac, in 2008.

Between the lines: In the absence of Sunday’s announcements, the insurance fund would have been pressed into heavy duty by the onset of an inevitable banking crisis.

Conversely, in the presence of the announcement, there’s no need for anybody to move their money at all, and the pressure on the fund could be tiny.

In other words: While this is undoubtedly a bailout of depositors at SVB and Signature, its cost could, weirdly, be negative.

What they’re saying: “The deposit insurance fund is bearing the risk,” a senior administration official told reporters on Sunday. “This is not funds from the taxpayer.”

What they’re not saying: Most taxpayers are also bank depositors, and some portion of their bank deposits is used to fund the FDIC, in what feels much like an involuntary tax being levied by a government agency.

The bottom line: If a bailout doesn’t cost anything, is it really a bailout?

https://www.axios.com/2023/03/13/let-the-bailout-debate-begin-silicon-valley-bank-fdic

Install a clown, expect a circus

It all circles back to election fraud.

Is this a move to Nationalize banks?

Or are we bailing out China/American investment

More the latter.

A guest yesterday on meet the depressed said the quiet part out loud. She said SVB was essentially a democrat ATM

We are sure to see Mitch want that bail out.

How much money is in the” FDIC?

how long before we see bail ins, where depositors see a portion of their savings taken?

Former BlackRock employee believes that the economic bubble is going to burst soon. He thinks the covid passports and medical tyranny are so the system has measures in place to deal with the rioting that would result from economic collapse.

The FDIC has 125 billion on hand. SVB has in excess of 264 billion in deposits.

I would say the FDIC is under water

And by guaranteeing all deposits across all banks, they committed themselves to over 19 trillion in deposits.

a 5 billion dollar loan out, collateral? Wine…lets have a partay!

Since many of these banks you mentioned stopped trading today are NOT WOKE, I wonder if a pattern will emerge as clear as joe’s two-tiered justice system.

You know, bailouts for ours but not for yours.

Newsweek has the list and amounts of value dropped in one day:

https://www.newsweek.com/full-list-bank-shares-that-halted-trading-panic-spreads-1787426

this!