![]()

by Alasdair Macleod

In the war between the western alliance and the Asian axis, the media focus is on the Ukrainian battlefield. The real war is in currencies, with Russia capable of destroying the dollar…

So far, Putin’s actions have been relatively passive. But already, both Russia and China have accumulated enough gold to implement gold standards. It is now overwhelmingly in their interests to do so.

From Sergey Glazyev’s recent article in a Russian business newspaper, it is clear that settlement of trade balances between members, dialog partners, and associate members of the Shanghai Cooperation Organisation (SCO) optionally will be in gold. Furthermore, the Russian economy would benefit enormously from a decline in borrowing rates from current levels of over 13% to a level more consistent with sound money.

To understand the consequences, in this article the comparison is made between the western alliance’s fiat currency and deficit spending regime and the Russian-Chinese axis’s planned industrial revolution for some 3.8 billion people in the SCO family. China has a remarkable savings rate, which will underscore the investment capital for a rapid increase in Asian industrialisation, without inflationary consequences.

With a new round of military action in Ukraine shortly to kick off, it will be in Putin’s interest to move from passivity to financial aggression. It will not take much for him to undermine the entire western fiat currency system — a danger barely recognised by a gung-ho NATO military complex.

Introduction

In the geopolitical tussle between the old and new hegemons, we see the best of strategies and the worst of strategies, where belief is pitted against credulity. It is the season of light and the season of darkness, the spring of hope and the winter of despair…

Recalling some of Charles Dickens’ famous opening lines from his Tale of Two Cities to describe the current state of global politics sums up the potential of a new industrial revolution throughout Asia and much of the rest of the under-developed world (the best of times), compared with the western alliance abetted by its military arm, NATO, which is determined to suppress the plans for the new hegemons at its own peoples’ expense (the worst of times). Ironically, the nations which will benefit most from the western alliance’s proxy war are those which align themselves with its enemies.

Plus ça change. But we must leave Dickens and look more closely at our modern situation — whereby America’s finance and currency-based hegemony has outlasted its benefits to the world order. We must recognise that a new order has been emerging since the Russian counter-revolution of 1989 when the Berlin Wall fell and in China following the death of Mao. For over thirty years, there has been the prospect of a new economic liberation for not just Russia and China, but almost the entire underdeveloped world. The tale of two worlds is about the governments of the established 1.2 billion souls in the so-called advanced economies, determined to contain the other 6.7 billion from challenging it. It is a clash between production-based economies, and economies increasingly based on services and finance. It is a clash between real values and ethereal values. It is evolving into a clash between fiat currencies and sound money.

Ukraine, and the role of Germany

Today, the clash of the hegemons is focused on Ukraine. It has already shifted from Afghanistan, and before that, Syria. Every time, America which runs NATO and the five-eyes intelligence network has failed to defeat the Asian axis because of their refusal to be drawn into outright conflict. Apart from defending their direct interests, Russia and China have watched NATO gently fall apart. First, it was the British refusing to support an all-out conflict in Syria. Then, it was Turkey, a NATO member which has understandably seen its interests to lie more in line with the Asian hegemons. Will Germany be next?

The fear in Washington must be whether Germany will similarly pursue its very obvious commercial interests by aligning itself more with Russia and China, and less with her NATO masters. We saw this conflict of interests in the undercurrent over Germany’s reluctance to permit NATO to deploy Leopard tanks in Ukraine. This has been sold to us as a reluctance to send German weapons into a theatre of war last invaded by the Nazis. Undoubtedly, it did stir up some unpleasant memories, but the whole ethos of post-Berlin-Wall Germany has been the peaceful development of its own commercial interests to the east.

For the Russian and Chinese axis, the restoration of commercial relations with Germany’s manufacturing-based economy would be of obvious mutual benefits. Equally, it would lead to the death of the EU in its current form. Perhaps it is Germany’s position in all this which is driving America and its NATO establishment towards do-or-die conflicts over Ukraine.

We should take a step back and look at this from Germany’s point of view. Since her defeat in the Second World War, Germany has been central to NATO’s existence. As Lord Ismay, NATO’s first secretary general pithily put it, its purpose was to keep the Soviet Union out, the Americans in, and Germany down. And with the history of the Ribbentrop-Molotov pact still in the back of everyone’s mind, it still summarises the situation today. From America’s point of view, while NATO was the military solution to Europe, the political situation could only be resolved by ensuring Germany was tied into Western Europe.

There were several claims as to who the Father of a United Europe was, but the version which triumphed was authorised by the American Committee on United Europe (ACUE), which was set up in 1948 by senior American intelligence figures from the CIA.[i] Germany is still kowtowing to US intelligence seventy-five years later.

But as the recent episode over Leopard tanks has shown, there is some resistance to this status quo. We also know that other Germans at high levels have been unhappy with the ECB’s monetary regime. Jens Weidmann, who resigned as President of the Bundesbank in October 2021, is not the only critic of monetary policy, though the Bundesbank now appears to have been purged of critics of the ECB.

Therefore, there are two issues holding back Germany. It has been forced to abandon its sound money principals, and to cut itself off from its natural markets in Asia. But a resumption of NATO backed hostilities will throw Germany’s suppression by the US political and military establishments into sharp relief. Chancellor Scholtz will know that Russia is highly unlikely to be easily defeated. If anything, this forthcoming NATO venture is the western alliance’s final desperate throw of the dice. And despite NATO, Scholtz must keep his options open.

If against all alliance propaganda NATO fails to win in Ukraine, Russia consolidates its position, and Putin remains as a strong Russian leader, Germany must be prepared for a political accommodation with Russia. It is not only a question of geographical proximity, but Germany has a strong manufacturing ethos, benefitting from access to Russian resources, markets for its products, and through Russia renewed access and cooperation with China.

Clearly, Germany’s commercial ethos has more in common with the industrial revolution being planned by the Asian axis and their emerging plans for sound money than it has with most of her EU partners. If only Germany was free of US political control, in time she could establish a new Hanseatic League, a trade corridor from Eastern Europe encompassing the Baltics and Netherlands. It is considerations of this sort that must make the US establishment determined to not release its grip over Germany and the wider EU.

There is no obvious basis for a truce over Ukraine

There has been some hope expressed that before a new conflict escalates, a truce will be called leading to peace negotiations. Less gung-ho voices have called for negotiations, notably that of Henry Kissinger. There will have been some back-channel meetings as well, such as that between William Burns of the CIA, and Sergei Naryshkin, head of Russia’s foreign intelligence agency in Ankara last November.

According to Pepe Escobar, who is probably the most seasoned reporter on these matters not employed in western mainstream media, only this week the Americans have made “an offer the Russians cannot refuse”[ii]. It was spelled out in a Washington Post Op-Ed, bypassing Kiev entirely, offering to partition Ukraine along with a deal for a post-war military balance. The trouble with this approach is that the Americans have a track record of making promises to Russia only to be broken later. Most notably, in February 1990 US Secretary of State James Baker promised Mikhail Gorbachev that NATO’s expansion would not be “one inch eastwards”, and was one of “a cascade of similar promises”[iii].

Not only does Russia mistrust the Americans, but in the chess board of international diplomacy, moves being initiated by the Americans puts Russia is in the stronger position. Peace talks initiated by the Americans would almost certainly require them to bend to Russian demands, just as if Russia initiated peace talks, she would be in the weaker position. Whether America is prepared to concede its control over Western Europe will become the central issue. The Russians are likely to insist on it. It would be the end of NATO, and a new European defence alliance without American involvement would have to take its place.

Furthermore, in the absence of an agreement Russia would be comfortable letting NATO continue to tie itself in knots. To the independent observer, the western alliance’s commitment to defeat Russia in a Ukrainian proxy war was a strategic blunder, pregnant with unintended consequences. It was a failure on the scale of the US’s intelligence failings over Iraq’s weapons of mass destruction. This time, the mistake was to underestimate the strength of Russia’s economy and her financial position.

Sanctioning her was meant to cripple Russia, instead it crippled the western alliance while the rouble turned in the strongest currency performance in 2022. And western media still claims that Russia is suffering unaffordable losses of trade revenue, at a time of exceptional military expenditure.

Obviously, there is some truth in this. But Russia’s underlying economy is far healthier than we have been led to believe. And despite massive military spending commitments, last year Russia’s budget deficit was only 2.3% of GDP, compared with the US’s 5.4%. The economic consequences of war has benefited Russia through higher energy prices, while it has cost the western alliance in price inflation and higher interest rates. Russia should have no trouble financing a 2023 deficit of 2.3% or more by borrowing in domestic markets, without undermining the rouble, while the financial consequences for the alliance of a new conflict are potentially catastrophic.

From his statements, we can be sure than Putin and his advisers understand not only the military position, but the relative economic consequences of a renewed escalation of the Ukrainian conflict. This is in contrast with American-led NATO policies, where so far, the economic costs have been ignored. The potentially disastrous consequences for European economies do not appear to have been thought through. Instead, by shipping in tanks of various makes to the Ukrainians so that a new attack by proxy can be mounted on Russia, the western alliance is doubling down on its earlier mistakes.

The euro’s survival is now crucial

It is the consequences for the euro of a renewed battle over Ukraine that threaten to finally undo American influence in Europe, and therefore the future of both NATO and the EU. When the ground freezes enough in Eastern Ukraine for tank warfare (perhaps within weeks) a new conflict will begin — unless a pre-battle missile attack by Russia on Ukraine’s supply lines hasn’t already commenced by then. Anticipating the uncertainty that follows, energy prices are bound to rise again. On 24 February 2021, when Russia commenced its “special operations” the price of gold was $1902. By 9 March, it had risen to $2070. All other commodity prices from base metals to raw materials and food soared. There’s no reason to think it will be different this time.

The consequences for the alliance’s financial markets are potentially devastating. Kiss goodbye to transient inflation and interest rate moderation. Say hello to soaring bond yields, collapsing equity markets, bankrupt banking systems including the central banks themselves, and debt traps for both governments and overleveraged businesses. Fiat currencies will teeter on the precipice of collapse. A new phase in this war will threaten to destabilise the western alliance, but not Russia and China whose economies are not beholden to deflating financial sector bubbles.

There’s little doubt that the euro is particularly vulnerable to the consequences of a new military escalation in Ukraine and the effects it is bound to have on producer and consumer prices in the Eurozone. The euro is the vol-au-vent of fiat currencies, a currency at risk which demonstrably takes from Germany’s savers to fund the fiscally spendthrift PIGS. Rising interest rates and bond yields have done very little to offset increases in the general levels of producer and consumer prices. In the absence of a rapid defeat of Russia, a renewed escalation of the Ukrainian conflict is sure to drive those price levels even higher.

The ECB will be torn between the need to respond with yet higher interest rates for fear of losing control over them to market forces, and the consequences of permitting higher interest rates and bond yields for government finances. Not least, there is the threat to the solvency of the entire euro system.

The only solution, and even that is likely to be short-term, is for America to step back from the battle for Western Europe and recognise Russia’s right to protect the integrity of her borders. Negotiations leading to a settlement would have to be offered to Russia immediately if the euro is to be saved. Only then, the prospect of lower energy and commodity values feeding into producer and consumer prices would provide some relief for the euro system and the euro itself.

It would buy ssome time for the ECB, which along with the other central banks of the western alliance relies on unsound fiat currencies for economic management. This is in sharp contrast to an emerging Asia, characterised by commodity backed currencies, genuine production, and capital funded by consumer savings.

Economic consequences flow from a world riven into two halves: one financially and services driven and the other, production and resource driven. We must now look at these in turn.

Mounting problems for fiat currency economies

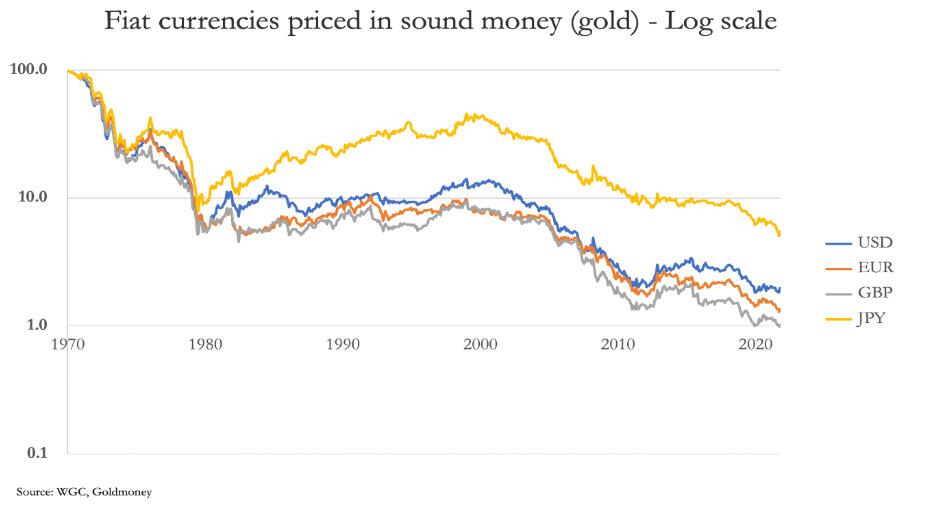

Since August 1971, when the last vestiges of a gold standard under the Bretton Woods agreement were abandoned by President Nixon, currencies in the advanced world were then managed with reference to the US dollar. From that time, the purchasing power of these currencies began to be eroded, to the point whereby today’s dollar is worth only 1.8 cents of the Bretton Woods dollar valued in legal money, which is still gold. The loss of purchasing power for the other currencies has been similar, as the chart below shows.

The loss of purchasing power for all these fiat currencies has become embedded into monetary policies, which aims to see an increase in the general level of prices by 2% every year. It is not a policy which can be implemented with any accuracy. Furthermore, it has led to governments condoning inflationary policies, and supplementing taxation by credit inflation at the central bank level.

The manipulation of currency values and monetary inflation is now the cornerstone of government finances, inevitably leading towards an existential crisis. In the belief that this was a problem that could always be resolved or continually deferred, members of the western alliance simply closed down economic activity over covid, in the belief that everything would subsequently revert to normality. That didn’t happen, and a period of supply chain disruption followed, requiring further deficit spending by governments with revenue shortfalls. The consequences of excessive currency expansion were in place to be triggered. Then there was the proxy war over Ukraine, and its economic effects for commodity, producer, and consumer prices.

The delusion of fiat currency economics has built up since the Bretton Woods agreement was abandoned. And the path to increasing dependence on inflationary policies had been eased by corrupting the statistics by which econometricians measured the consequences. The general level of prices is an unmeasurable concept, yet that has not stopped western governments constructing retail and consumer price indices. And because they are unmeasurable, government statisticians can come up with their own versions. The increasing use of inflation linking has encouraged reform of statistical composition, always succeeding in reducing the cost of inflation-linking to government finances. And in recent decades, it has offered the additional benefit of concealing the true consequences of monetary policy for currency debasement. The only reliable way of estimating the debasement of these currencies is to compare their value against gold, which is still legal money internationally, despite official protestations to the contrary.

The misuse of the gross domestic product statistic as the means of measuring economic activity or progress is another egregious example of economic dillusion. GDP is simply an estimate of total qualifying transactions and is not a reflection of how productive or relevant they are to progressing the human condition. Indeed, they include government spending, much of which we know to be wasteful and none of it can be said to be economically valued by consumer demand.

Instead, GDP is something that can be easily boosted by measures taken to increase the quantity of currency and credit, and by governments increasing their non-productive spending. And when you can control the statistical representation of the effect on prices, you appear to have achieved perpetual economic motion.

The prosecution of a new war between the superpowers has finally exposed the weaknesses and contradictions of the western alliance’s fiat currency system, threatening to bring forward the final realisation that it is fatally flawed. When an entire financial and economic system is at risk of failing, it is difficult to select one aspect which will bring the whole illusion down. It is easier to put the principal errors as topics in bullet form, so the reader can get a sense of the scale of the overall problem:

And the New York Slimes(Times)will be on the side of the Enemy since they have been since Walter Duranty was Stalin’s NYT’s Propagandists back in 1932