![]()

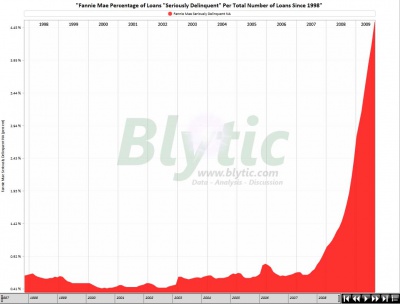

The [Fannie Mae] “seriously delinquent” rate has gone parabolic, increasing by roughly 5% sequentially and just under 300% YoY [year-over-year]. As mere text will simply not do this metric justice, please enjoy this chart of the dataset from Blytic. It tells you all you need to know about the Fed’s containment of the housing problem.

The August seriously delinquent single-family number comprised of a 2.87% non-credit enhanced delinquencies and a very bothersome 11.52%, consisting of credit enhanced loans

~~~The deterioration of FNM’s book however did not stop it from increasing the size of its book [loans]. In September Fannie’s total book of business hit $3.242 trillion, up from $3.229 trillion in August and $3.079 trillion in the prior year

~~~This trend should bother you, dear taxpayer, because it is your money on the hook here, which is not only massively mismanaged by Bernanke & Co., LLC, but which sees another $80 billion of free funding every month courtesy of the dollar printing press to onboard even more toxic garbage onto your balance sheet.

And who is paying the price?

“Absent any catastrophic home price decline, FHA will not need to ask Congress and the American taxpayer for extraordinary assistance—we will not need a bailout,” Mr. Stevens said in prepared testimony before a congressional panel on Thursday.

Concerns are growing because the agency’s annual audit, due to be released later this fall, will show that its projected reserves will fall below their federally mandated level. The FHA has a capital cushion of around $30 billion, and it has insured some $725 billion loans. The agency’s annual review estimates the value of its reserves after accounting for estimated losses on loans it has insured.

“It appears destined for a taxpayer bailout in the next 24 to 36 months,” mortgage-industry veteran Edward Pinto said in prepared testimony. He estimated that the agency faces losses of $70 billion on loans it has already made, leaving it short of its current reserves by around $40 billion. That estimate is modeled under the assumption that FHA-backed loans will perform similarly to loans made by Fannie Mae in 2006 to borrowers with low down payments.

But it’s all good to Barney Frank:

If many of the loans turn into pumpkins, that’s OK. House Financial Services Committee Chairman Barney Frank, D-Mass., actually told The New York Times, “I don’t think it’s a bad thing that the bad loans occurred. It was an effort to keep prices from falling too fast.” In other words, soaring defaults are not a bug. They’re a feature.

What can you even say to respond to such idiocy?

See author page

Get him out of there!

It’s the AGW hockey stick graph!

So to keep prices from falling, they made bad loans….

I keep re-reading that, but my brain STILL can’t make it into anything approaching logical.