![]()

Oh you have got to admire the ability of the media to shift gears from unquestioned and unbridled love to suddenly becoming a million microscopes of check and balance. You’ve also got to admire Pres-elect Obama’s ability to find quality people-people who will CHANGE Washington-not.

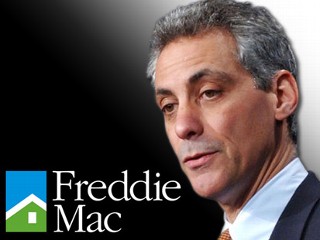

President-elect Barack Obama’s newly appointed chief of staff, Rahm Emanuel, served on the board of directors of the federal mortgage firm Freddie Mac at a time when scandal was brewing at the troubled agency and the board failed to spot “red flags,” according to government reports reviewed by ABCNews.com. According to a complaint later filed by the Securities and Exchange Commission, Freddie Mac, known formally as the Federal Home Loan Mortgage Corporation, misreported profits by billions of dollars in order to deceive investors between the years 2000 and 2002.

Emanuel was not named in the SEC complaint but the entire board was later accused by the Office of Federal Housing Enterprise Oversight (OFHEO)of having “failed in its duty to follow up on matters brought to its attention.”

Author of “Reparations and America’s 2nd Civil War

Reparations and America’s 2nd Civil War: Malensek, Scott: 9798864028674: Amazon.com: Books

How convenient to release this NOW that the Dems are responsible for Fannie & Freddie.

Mr. Emanuel received more than $335,000 from Fannie & Freddie as a member of the board as well as gimmies that he got as a Congressman.

Change!

Hope!

Nope.

Hope is done; accomplished. Now it’s time to put up or shut up. The left knows it. The media knows it. Obama knows it. I love it, and they’re confused/filled with aimless anger and opposition w no one to oppose.

Hussein will ‘change’ the flow of money into Hussein’s bank account.

I wasn’t aware that Freddie Mac collapsed in the 2000-2002 period. It seemed pretty much alive until September 2008.

Ralph, apparently (had you read the article) Rahm did not agree with your assessment. He in fact warned that it was in trouble, but…then he took some $300,000 from em later on, so…maybe you’re right. 😉

Sorry, Scott, but I read the article, and I didn’t see anywhere in it that Freddie was “collapsing” in the period Rahm was on the board. Nor did I see where the article stated that Rahm believed it was “collapsing”. In fact, the word “collapse” doesn’t appear in the article at all.

I think it’s your reading comprehension at fault here.

When did the collapse start? If you think Sept, then why the people chiming out about problems years ago? Seems the seeds were sown back when Rahm was Director.

I’ll change the “COLLAPSE” to “SCANDAL” for ya.

Fine with me. Thanks.

No problem Ralph. I actually appreciate your keeping me in check. I should’ve stuck closer to the original title. Sincerely appreciated (no bs).

🙂

btw, now you’re gonna have to keep coming to FA to keep on keepin me in check. Clearly I need you.

If that’s true, you’re in big trouble. But I’ve been lurking here for many moons.

We have known they wre going to crash as far back as 2001. Why do you think that Bush tried to reign it in back then. But it got the pass by the Dems and hapless Republicans. So yes we did know it was going to crash and kept on punting it down the line until it totally collapsed.

Hell, you can go back to 1998 when the CRA was put on steroids to see that this was coming.

http://abcnews.go.com/Politics/Story?id=6207491&page=2

– Larry W/HB

@Larry Weisenthal: Yes, Graham that stalawart of the Conservatives. He is even farther left than McCain is.

Larry,

“…honest, direct and candid…” Please! He is nothing at all like that. He is corrupted to the bones, he hides all his records and vicious friends (wonder why…lol), and he is everything but candid. You are more intelligent than that Larry to fall for that bullshit. Gee… you will find out soon whom the real Obama is.

Dear Mr. Obama: Who Are You?

http://www.disclose.tv/action/viewvideo/8971/Dear_Mr__Obama__Who_Are_You_/

Stix, the concept that the Community Reinvestment act had anything to do with the financial meltdown is not supported by the fact that not a single Republican made this into a campaign issue. The data prove otherwise:

Of all the sub-prime mortgages, only 1/4 to 1/3 were Fannie/Freddie-backed. Of all the subprime mortgages, only 9% were for owner-occupied first houses (CRA targets). Of all the money which went into sub-prime mortgages, less than 1% could possibly be CRA-related loans.

The financial crisis wasn’t caused by Fannie/Freddie, and it certainly wasn’t caused by the CRA. It’s mathematically impossible to believe that the CRA could have played any role, at all. Fannie/Freddie leadership made the same bad investments as the rest of the completely private financial sector (who made 2/3 to 3/4 of the bad loans and sold off and bought the mortgage-related paper, totally unbacked by Fannie/Freddie. The investment decisions of Fannie/Freddie were motivated by the desire to make profits for their shareholders, just as in the case of the non-government related financial institutions, who were responsible for 2/3 to 3/4 of the total action.

The proximate cause of the crisis was a capital glut, chasing too few investment opportunities, which created a demand for exotic securities.

Again, this is the reason why no politicians tried to make a big issue out of the meltdown, in terms of blaming Fannie, Freddie, and especially the CRA.

– Larry Weisenthal/Huntington Beach

@Larry Weisenthal: Are you for real. readthtough some of the archives here and tell me CRA had nothing to do with it.

they did not use the CRA because both Repubicans and Democrats had ther hands in the cookie jar.

Another thing that btounght onthe meltdown was Alan Greenspan cuting the rates everytime there was a hint of inflation and just punted the meltdown down the road. we never had a correction because the geovernment stuck its hand in the Free Market too many times. The Market goes up and down naturally, but the goevnernment stoppedthe natural flow with stupid policies.

@stix1972:

Larry is the only one convinced by his arguments.

He can say what he wants to say but those darned facts sure are stubborn things.

@Aye Chihuahua: Yes I agree

My brother almost puts all the blame on Greenspan. But I think that forcing loans on banks had a great effect also. And the government kept putting its hand into something that it should not have.

Larry,

No wonder you vote for THE ONE you do not understand that subprime crisis. I will try to find you a convincing article from the best Economists in this world to prove you wrong. I have a couple here but they are all in French. To bad Friedman is dead; he would have explained it perfectly for you. Government’s regulations in economy always screws-up economy… that is the first rule of capitalism.

McCain hardly pointed it out because McCain wants to be the “good guy”. Unfortunately, good guys always lose. Good guys are eternal losers.

Now now, Craig. The correct term is not “the one”, but “*that* one”….. LOL

For the debate version…

For the stellar comedy version… highly recommended! (because “smiles” are so danged rare in politics….)

Beware…. the left is spinning this as “racist” … with the new terminology of “otherness” LOL

Larry… INRE your comment

I just can’t let you get away with this, guy. A claim that CRA had nothing to do with our financial status today is not “supported” by fact because not a single GOPer made this into a campaign issue is just plain absurd.

First of all, CRA new compliance regs, rewritten on the sly by Clinton’s Treasury Secy Rubin, may not be the entire problem, but it was the starting point of the “perfect storm” of event.s

Secondly, the truth not only hurts, but can be spun. Shall I do it for you?

Issuing loans to unqualified minorities is a bad thing for the market. You might as well bundle arsenic cookies and market them thru your local food chain. The problem is not distribution… but distributing arsenic cookies.

Now… let’s see the GOP try to convince the electorate that giving minorities loans… even unqualified.. is a good campaign tactic.

It’s true, but it’s a losing proposition. Easier to blame it on securitization. But not truth. Just politically correct.

Larry,

Here is a good artivle that should help you to understand the subprime crisis:

THE REAL CULPRITS IN THIS MELTDOWN

By INVESTOR’S BUSINESS DAILY

Posted Monday, September 15, 2008

Big Government: Barack Obama and Democrats blame the historic financial turmoil on the market. But if it’s dysfunctional, Democrats during the Clinton years are a prime reason for it.

Obama in a statement yesterday blamed the shocking new round of subprime-related bankruptcies on the free-market system, and specifically the “trickle-down” economics of the Bush administration, which he tried to gig opponent John McCain for wanting to extend.

But it was the Clinton administration, obsessed with multiculturalism, that dictated where mortgage lenders could lend, and originally helped create the market for the high-risk subprime loans now infecting like a retrovirus the balance sheets of many of Wall Street’s most revered institutions.

Tough new regulations forced lenders into high-risk areas where they had no choice but to lower lending standards to make the loans that sound business practices had previously guarded against making. It was either that or face stiff government penalties.

The untold story in this whole national crisis is that President Clinton put on steroids the Community Reinvestment Act*, a well-intended Carter-era law designed to encourage minority homeownership. And in so doing, he helped create the market for the risky subprime loans that he and Democrats now decry as not only greedy but “predatory.”

Yes, the market was fueled by greed and overleveraging in the secondary market for subprimes, vis-a-vis mortgaged-backed securities traded on Wall Street. But the seed was planted in the ’90s by Clinton and his social engineers. They were the political catalyst behind this slow-motion financial train wreck.

And it was the Clinton administration that mismanaged the quasi-governmental agencies that over the decades have come to manage the real estate market in America.

As soon as Clinton crony Franklin Delano Raines took the helm in 1999 at Fannie Mae, for example, he used it as his personal piggy bank, looting it for a total of almost $100 million in compensation by the time he left in early 2005 under an ethical cloud.

Other Clinton cronies, including Janet Reno aide Jamie Gorelick, padded their pockets to the tune of another $75 million.

Raines was accused of overstating earnings and shifting losses so he and other senior executives could earn big bonuses.

In the end, Fannie had to pay a record $400 million civil fine for SEC and other violations, while also agreeing as part of a settlement to make changes in its accounting procedures and ways of managing risk.

But it was too little, too late. Raines had reportedly steered Fannie Mae business to subprime giant Countrywide Financial, which was saved from bankruptcy by Bank of America.

At the same time, the Clinton administration was pushing Fannie and her brother Freddie Mac to buy more mortgages from low-income households.

The Clinton-era corruption, combined with unprecedented catering to affordable-housing lobbyists, resulted in today’s nationalization of both Fannie and Freddie, a move that is expected to cost taxpayers tens of billions of dollars.

And the worst is far from over. By the time it is, we’ll all be paying for Clinton’s social experiment, one that Obama hopes to trump with a whole new round of meddling in the housing and jobs markets. In fact, the social experiment Obama has planned could dwarf both the Great Society and New Deal in size and scope.

There’s a political root cause to this mess that we ignore at our peril. If we blame the wrong culprits, we’ll learn the wrong lessons. And taxpayers will be on the hook for even larger bailouts down the road.

But the government-can-do-no-wrong crowd just doesn’t get it. They won’t acknowledge the law of unintended consequences from well-meaning, if misguided, acts.

Obama and Democrats on the Hill think even more regulation and more interference in the market will solve the problem their policies helped cause. For now, unarmed by the historic record, conventional wisdom is buying into their blame-business-first rhetoric and bigger-government solutions.

While government arguably has a role in helping low-income folks buy a home, Clinton went overboard by strong-arming lenders with tougher and tougher regulations, which only led to lenders taking on hundreds of billions in subprime bilge.

Market failure? Hardly. Once again, this crisis has government’s fingerprints all over it.

http://www.ibdeditorials.com/IBDArticles.aspx?id=306370789279709

Here is the rest of the article above:

… Tough new regulations forced lenders into high-risk areas where they had no choice but to lower lending standards to make the loans that sound business practices had previously guarded against making. It was either that or face stiff government penalties.

The untold story in this whole national crisis is that President Clinton put on steroids the Community Reinvestment Act*, a well-intended Carter-era law designed to encourage minority homeownership. And in so doing, he helped create the market for the risky subprime loans that he and Democrats now decry as not only greedy but “predatory.”

Yes, the market was fueled by greed and overleveraging in the secondary market for subprimes, vis-a-vis mortgaged-backed securities traded on Wall Street. But the seed was planted in the ’90s by Clinton and his social engineers. They were the political catalyst behind this slow-motion financial train wreck.

And it was the Clinton administration that mismanaged the quasi-governmental agencies that over the decades have come to manage the real estate market in America.

As soon as Clinton crony Franklin Delano Raines took the helm in 1999 at Fannie Mae, for example, he used it as his personal piggy bank, looting it for a total of almost $100 million in compensation by the time he left in early 2005 under an ethical cloud.

Other Clinton cronies, including Janet Reno aide Jamie Gorelick, padded their pockets to the tune of another $75 million.

Raines was accused of overstating earnings and shifting losses so he and other senior executives could earn big bonuses.

In the end, Fannie had to pay a record $400 million civil fine for SEC and other violations, while also agreeing as part of a settlement to make changes in its accounting procedures and ways of managing risk.

But it was too little, too late. Raines had reportedly steered Fannie Mae business to subprime giant Countrywide Financial, which was saved from bankruptcy by Bank of America.

At the same time, the Clinton administration was pushing Fannie and her brother Freddie Mac to buy more mortgages from low-income households.

The Clinton-era corruption, combined with unprecedented catering to affordable-housing lobbyists, resulted in today’s nationalization of both Fannie and Freddie, a move that is expected to cost taxpayers tens of billions of dollars.

And the worst is far from over. By the time it is, we’ll all be paying for Clinton’s social experiment, one that Obama hopes to trump with a whole new round of meddling in the housing and jobs markets. In fact, the social experiment Obama has planned could dwarf both the Great Society and New Deal in size and scope.

There’s a political root cause to this mess that we ignore at our peril. If we blame the wrong culprits, we’ll learn the wrong lessons. And taxpayers will be on the hook for even larger bailouts down the road.

But the government-can-do-no-wrong crowd just doesn’t get it. They won’t acknowledge the law of unintended consequences from well-meaning, if misguided, acts.

Obama and Democrats on the Hill think even more regulation and more interference in the market will solve the problem their policies helped cause. For now, unarmed by the historic record, conventional wisdom is buying into their blame-business-first rhetoric and bigger-government solutions.

While government arguably has a role in helping low-income folks buy a home, Clinton went overboard by strong-arming lenders with tougher and tougher regulations, which only led to lenders taking on hundreds of billions in subprime bilge.

Market failure? Hardly. Once again, this crisis has government’s fingerprints all over it.